“Shocking Levels Of Distress”: CMBS Delinquencies Unexpectedly Soar To Covid Highs

With market focused on private credit as the next credit market crisis vortex, many have forgotten that CMBS, the asset class that was smashed in the aftermath of covid as hundreds of office buildings were suddenly left vacant, has been teetering on the edge for years. For some, it proved to be a lucrative bet as the “next big short” after various office-heavy CMBX tranches collapsed in 2020 and 2021. But due to the slow-burning nature of commercial real-estate deterioration, where data center REITs provided a solid offset to weakness elsewhere, credit markets eventually moved on to the next worst thing.

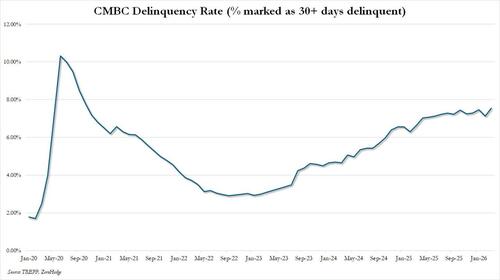

It may be time to reassess: according to the latest TREPP CMBS monthly report, March saw a surge in the delinquency rate, which jumped by 41bps to 7.55%, the highest in years, led by a surge in the lodging rate, a category which until now was not a source of concern.

{kind=link}

TREPP states that the five largest newly delinquent loans accounted for just over $2 billion of the almost $5.1 billion in newly delinquent loans, including a West Coast hotel portfolio, a Midwest office loan, a Northeast retail center loan, a national hotel portfolio, and a Pacific Northwest office portfolio, which pushed the rate higher.

In addition, roughly 40% of the newly delinquent loans this month were considered performing matured balloon last month. Continuing the sideways delinquency trend as loans mature, go delinquent, cure, and become delinquent again.

Among all newly delinquent loans, non-performing matured balloon was the most common delinquency classification, consistent with prior months.

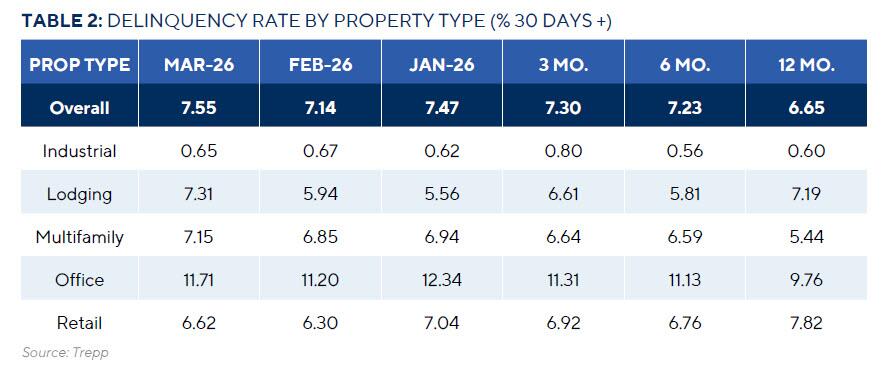

At the property-type level, four of the five major property type rates increased while one edged down slightly. Lodging posted the largest increase, jumping 137 basis points to 7.31%, the first time it has been above 7% since its recent April 2025 peak of 7.85%. Office rose 51 basis points to 11.71%, maintaining the elevated range established over the past year, but remaining below January 2026’s recent high of 12.34%. Retail increased 32 basis points to 6.62%, rising from February’s recent low of 6.30% but remaining below the higher readings observed in 2024 and early 2025, when that rate averaged 6.71%. Multifamily was also especially week, as the delinquency rate rose 30 basis points to 7.15%, pushing slightly above its prior high-water mark of 7.12% in October 2025, and well past its marks from one year ago of 5.44% and 1.84% two years ago. Industrial – a stable category which includes warehouse and data center REITs – dipped slightly to 0.65% from 0.67%, continuing to sit near the bottom of the major property-type delinquency spectrum.

{kind=link}

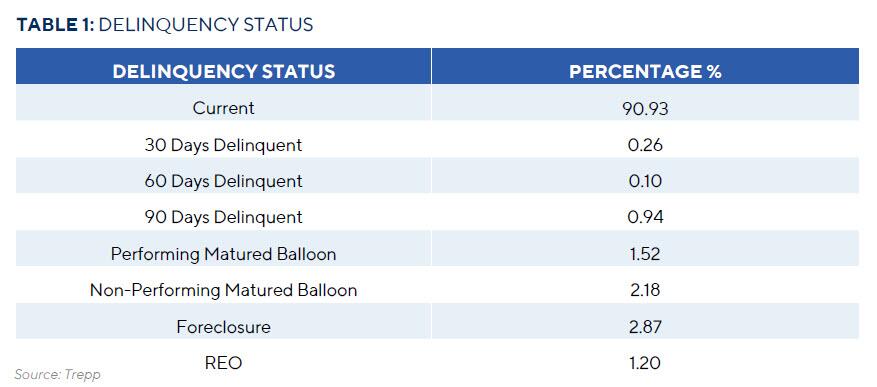

And in an ominous twist, if loans past their maturity date but current on interest (classified as performing matured balloon) were included, the delinquency rate would register 9.07%, up 32 basis points from February. This figure sits 152 basis points above the headline rate of 7.55% and continues to highlight the role of maturities in overall CMBS performance. The seriously delinquent rate (60+ days delinquent, in foreclosure, REO, or non‑performing balloons) also increased, rising to 7.29% (from 6.89%). The percentage of loan balance in the 30-day delinquent bucket is 0.26%, essentially flat versus February (0.25%).

{kind=link}

In a well-timed report, the WSJ yesterday published a reminder that much of the battered US office market continues to drag along the bottom, and continues to hold a fire sale, featuring some buildings marked down by more than 90%.

Some striking examples:

In Chicago, real-estate developer Marc Calabria bought a 485,000-square-foot office building for $4 million. The building sold for $68.1 million a decade ago.

Developer Asher Luzzatto paid a mere $5.3 million for the Denver Energy Center, after a foreclosure process. The two-building complex sold for $176 million in 2013.

Even the federal government’s landlord is getting in on the act. The General Services Administration last month sold a 940,000-square-foot building to a residential converter for $24 million, a tiny fraction of its value a few years ago.

Investors purchased 204 distressed office buildings nationwide last year, up from 133 sales in 2024, according to data firm MSCI. Sales of these properties, which were auctioned out of bankruptcies or sold through foreclosures and lender seizure, came to $5.2 billion. In the first two months of this year, sales volume of distressed offices was $808 million, up 24.5% from the same period last year, MSCI said.

{kind=link}

The bottom line is this: we may be approaching the next commercial real estate crisis because much of the reserves that kept the sector semi-solvent for years, have run out. As the WSJ puts it, “landlords and their lenders held on to their office towers for years, hoping for a turnaround after Covid. Now, they are accepting enormous losses. Owners and creditors are capitulating to the reality that more employees are splitting their work time between home and office. They are also resigned to stubbornly higher interest rates, which lower property values and make it harder for buyers to borrow.”

“People who don’t know real estate would be shocked at the level of distress,” Luzzatto said.

Of course, not every office building goes for a few pennies on the dollar. These are mostly B-grade, or poorer-quality buildings, often in undesirable locations. And owners of high-end office towers in the best locations of New York City and the hottest parts of San Francisco are raising rents and selling buildings profitably (although pockets of weakness are appearing there too, now that AI is making a growing number of tech workers obsolete).

But most office sales reflect the sector’s steep decline. Even higher-quality properties on average have dropped about 35% in value from their peak, according to analytics firm Green Street.

Buyers, meanwhile, are picking up office towers in major U.S. cities for roughly the price of a three-bedroom condo unit in Manhattan. These distressed sales are paving the way for new owners to pursue redevelopment ideas that would have been unthinkable just a few years ago.

Calabria in Chicago plans to convert the office building into an urban farm and education center. He is working with Farmzero, which will use grow lights and hydroponic farming techniques to produce millions of pounds a year of berries, tomatoes, lettuce, herbs and other vegetables.

“The buy-in at this distressed price allows us the opportunity to afford change,” Calabria said.

Rock-bottom prices are also accelerating the move to residential conversion. Developers who bought at steep discounts can now justify costly structural changes – such as carving out atriums or reconfiguring floor layouts – that would have been financially unworkable at higher valuations.

At the start of the year, more than 90,000 apartments nationwide were in the process of conversion nationwide, up 28% from a year earlier, according to data firm RentCafe. New York City’s obsolete buildings are leading the way, but tax breaks and other government incentives are helping spark similar projects in Chicago and Washington, D.C.

This reckoning follows years when office owners and their lenders avoided confronting the sector’s problems. Owners would inject more equity, while lenders extended loans in hopes of a rebound.

Now, with many concluding that values aren’t coming back, lenders are increasingly demanding repayment or selling the properties, a sign that the office market’s long slide that intensified during the pandemic is nearing a bottom.

“We’re six years from the shock of Covid,” said Jim Costello, an MSCI executive director. “But that’s how long it takes someone to capitulate and give up such a highly valued asset.”

The good news is that the threat of systemic risk remains low for now: many banks and other lenders are better positioned to take losses after spending the past few years shoring up their balance sheets and building reserves against troubled loans. Special servicers overseeing distressed office buildings financed through commercial mortgage-backed securities are also selling. The Chicago building being converted into an urban farm was sold by special servicer CW Asset Management, which said the low price was justified because the empty building’s taxes, utility bills and other costs were so high.

It isn’t just weak demand from remote work forcing down values. Owners must contend with the high cost of leasing up empty space -through hefty brokerage commissions and tenant incentives – and uncertainty about how AI could reshape office usage.

Sharp discounts are showing up in both downtown and suburban markets. For example, Newmark Group brokered the sale of five suburban Texas office buildings over the past two years at prices more than 50% lower than prepandemic values. Buyers demolished them to make way for higher-demand uses like industrial space.

Some of the big buyers of distressed office assets include Cross Ocean Partners, a credit-focused investment firm known for moving from one pocket of distress to another. It recently raised the first $300 million of a $750 million fund to buy distressed office assets—both debt and equity—in such markets as Minneapolis, Austin, Texas, and the Boston area.

The strategy centers on acquiring assets at steep discounts and underwriting the cash flow from existing tenants. Even if office demand remains weak, those in-place rents can generate a profit.

While institutional investors have largely pulled back from distress to focus on the strongest buildings in the most resilient markets, high-net-worth individuals are stepping in.

Hossein Fateh recently bought a 940,000-square-foot GSA building in Washington, D.C. A data-center investor, he made a fortune when Digital Realty paid $7.6 billion for DuPont Fabros Technology, which he co-founded.

Fateh is planning a residential conversion, adding a swimming pool or atriums in the middle of the floors to create windows. Such architectural hacks will help push the conversion cost into the hundreds of millions of dollars.

If the price wasn’t so low, “this deal wouldn’t work,” he said.

And with AI set to unleash the next big wave of office vacancy, coupled with banks throwing in the towel on cash-burning properties, many more such deals are emerging on the horizon.

Tyler Durden

Wed, 04/08/2026 – 21:20

0 comments on ““Shocking Levels Of Distress”: CMBS Delinquencies Unexpectedly Soar To Covid Highs” Add yours →