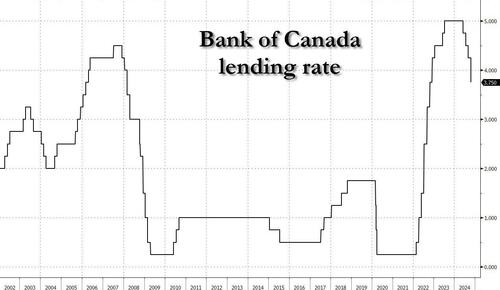

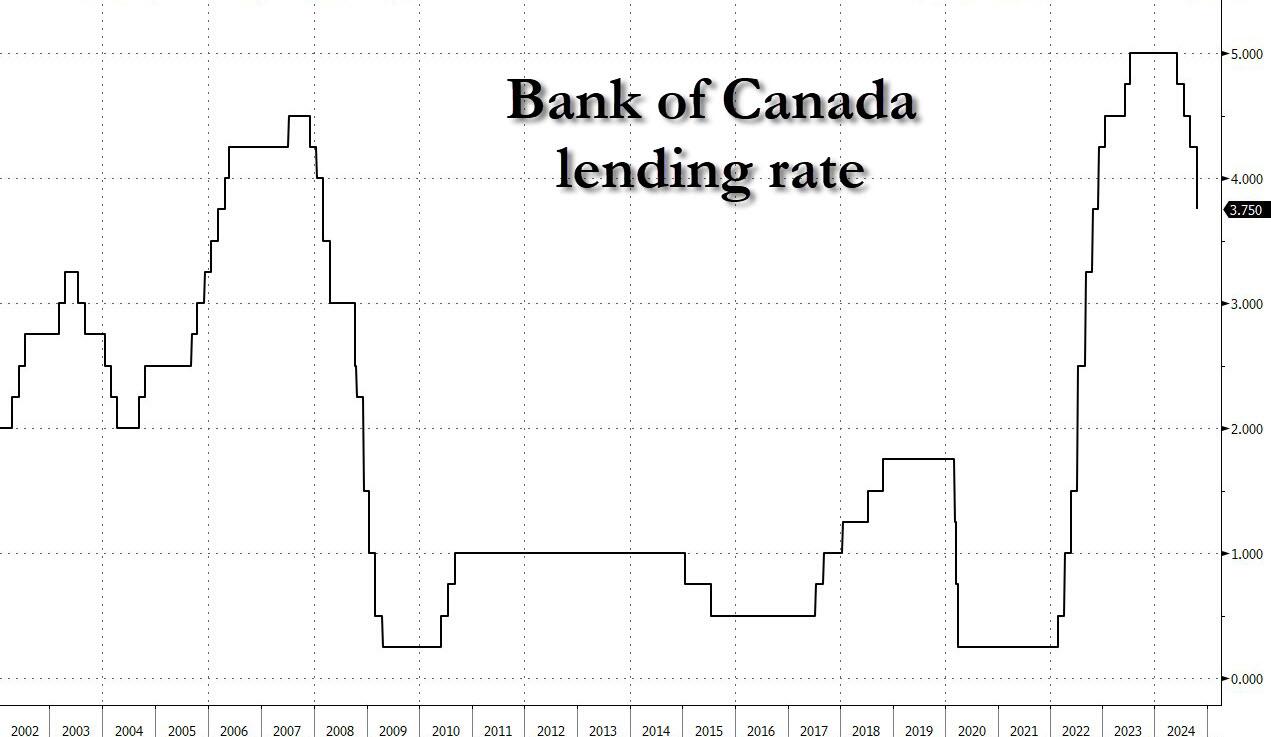

Bank of Canada Slashes Rates For 4th Straight Month In Biggest Rate Cut Since Covid

In keeping up with the global easing frenzy, and also in keeping with its promises from last month when it said to “expects further cuts”, moments ago the Bank of Canada – home of what may be the world’s biggest housing bubble – stepped up the pace of interest-rate cuts and signaled that the post-pandemic era of high inflation is over when the central bank cut the benchmark overnight rate to 3.75% on Wednesday, the biggest reduction in borrowing costs since March 2020 during the early days of the pandemic.

The Bank of Canada started easing borrowing costs with a quarter percentage-point reduction in June. It cut again by 25 basis points at each meeting in July and September. The next and final rate decision for this year is on Dec. 11, when some economists already project another 50 basis-point cut.

{kind=link}

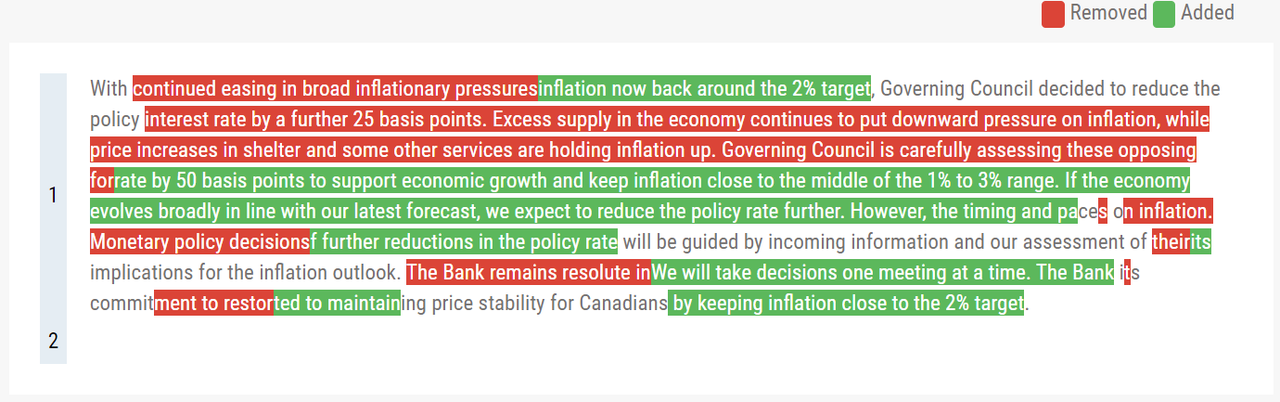

Here is a redline comparison of the BOC’s statement vs last month (courtesy of Newsquawk):

{kind=link}

Here are some highlights from the decision:

On Rates:

“the timing and pace of further reductions in the policy rate will be guided by incoming information.”

“We will take decisions one meeting at a time”.

CPI:

The Bank’s preferred measures of core inflation are now below 2%.

With inflationary pressures no longer broad-based, business and consumer inflation expectations have largely normalized.

Growth:

GDP growth is forecast to strengthen gradually over the projection horizon, supported by lower interest rates.

This forecast largely reflects the net effect of a gradual pick up in consumer spending per person and slower population growth

The jumbo cut – which was widely expected by markets and economists – aims to boost economic growth and keep inflation close to the 2% target in an economy where headline price pressures slowed to 1.6% in September and are no longer as broad, with inflation expectations now trending closer to normal.

The 50 basis-point cut suggests a new phase of monetary policy easing, where policymakers focus on returning interest rates to more neutral levels — where borrowing costs neither restrict nor stimulate growth — to avoid slowing the economy too much and having inflation undershoot the target.

“All this suggests we are back to low inflation,” BOC governor Tiff Macklem said in his prepared opening remarks. “Now our focus is to maintain low, stable inflation. We need to stick the landing.” The bank now sees upward and downward risks to its inflation projection as “reasonably balanced,” he added “but with inflation back to 2%, we want to see growth strengthen. Today’s interest rate decision should contribute to a pickup in demand.”

Here are some more highlights from his comments:

“We also expect growth in residential investment to rise as strong demand for housing lifts sales and spending on renovations.”

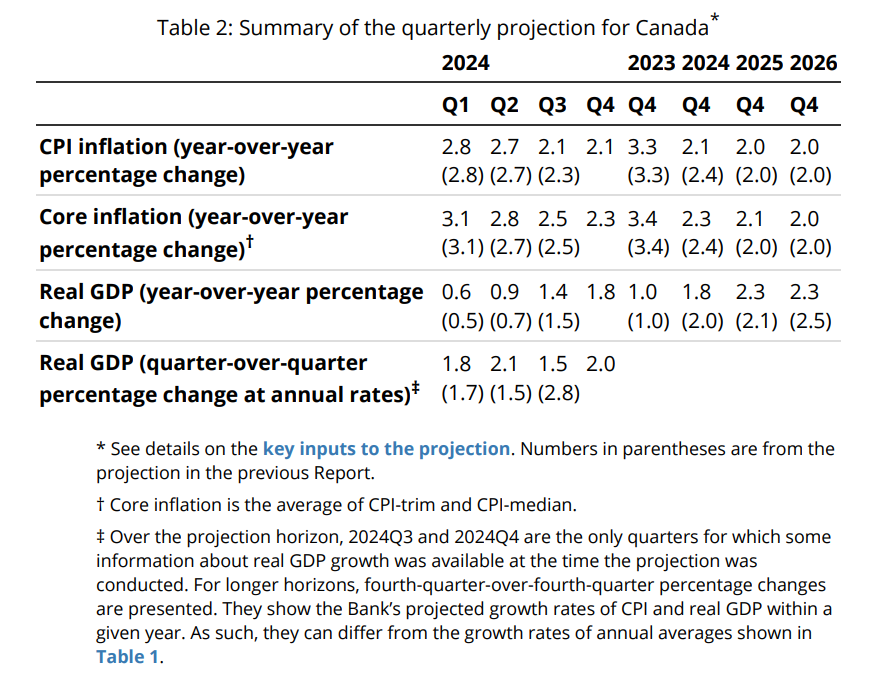

“Looking ahead. GDP growth is forecast to gradually strengthen to around 2% in 2025 and 2%% in 2026, supported by lower interest rates. This forecast largely reflects the net effect of a gradual pick up in consumer spending per person and slower population growth.”

“With stronger demand, the downward pressure on inflation is also forecast to dissipate, keeping the upward and downward forces roughly balanced.”

“Going forward, we can expect to continue to see some monthly fluctuations in inflation.”

“Overall, we view the risks around our inflation forecast as reasonably balanced. With inflation back to 2%. we are now equally concerned about inflation coming in higher or lower than expected. The economy functions well when inflation is around 2%.”

Hilariously, just like every other central bank, the Bank of Canada’s latest forecasts see policymakers achieving a soft landing, where inflation normalizes without a deep economic downturn. GDP growth, which is expected to be just 1.2% this year, should accelerate next year to just over 2%, while inflation is expected to remain near the midpoint of the 1% to 3% target range, the central bank said. Just like magic.

“We want to see growth strengthen. Today’s interest rate decision should contribute to the pickup in demand,” Macklem said. “We took a bigger step today because inflation is now back to the 2% target and we want to keep it close to the target.”

BOC officials said they expect to reduce the policy rate further if the economy evolves in line with their expectations, but they cautioned that the “timing and pace” of future cuts will be based on incoming data.

Before the release, traders in overnight swaps were betting the Bank of Canada would lower its policy rate to about 2.75%, the mid-point of the so-called neutral range, by September 2025.

In the monetary policy report accompanying the rate statement, the bank said headline inflation will remain close to the 2% target through 2026, with core measures of consumer prices easing gradually. The upward inflationary pressures from shelter and services are also forecast to further diminish.

While economic growth in the second quarter was slightly stronger than July’s forecast, the third quarter appears to be weaker, the report said. The bank said the economy continues to be in excess supply — wherein there isn’t enough demand for goods and services being produced — and the labor market is still soft, with population increases exceeding job creation.

Growth is expected to accelerate and average 2.25% over 2025 and 2026. Consumer spending and business investment are forecast to strengthen, supported by interest-rate decreases.

{kind=link}

Population growth is also expected to slow due to Prime Minister Justin Trudeau’s measures to curb the flood of immigrants.

Looking at the market reaction, the USDCAD was virtually unchanged as the decision and commentary were both very much as expected. Money markets now price in 31bps of Dec rate cuts (up from 30bps before the decision) and 60bps by January (up from 58bps).

Tyler Durden

Wed, 10/23/2024 – 10:06

0 comments on “Bank of Canada Slashes Rates For 4th Straight Month In Biggest Rate Cut Since Covid” Add yours →